The Silent Heartbreak of a Rejected Insurance Claim

Imagine this: You have paid your premiums faithfully for years. You never missed a single payment. You felt safe knowing that if something went wrong, your insurance company would be there to catch you. Then, the unexpected happens. Maybe a storm damages your roof, or you get into a car accident that wasn't your fault.

You file your claim with confidence. You wait. But instead of a check, you get a letter. "Claim Denied." Your heart sinks. You feel a mix of anger and pure fear. How could this happen? You did everything right, or so you thought.

This is a reality for thousands of people every single day. The mental stress is overwhelming. You are already dealing with a crisis, and now you have a financial mountain to climb alone. It feels like the system is rigged against you. You start questioning your choices and your future.

"Was I not covered for this?" you ask yourself. The truth is often more complicated than a simple "yes" or "no." Most people think insurance is a straightforward deal. You pay money, they cover the loss. But behind the scenes, there are tiny details that can pull the rug out from under you.

I have seen families lose their savings because of a single sentence in a document they didn't read. It isn't just about the big things; it’s about the hidden factors you never even noticed. It is about the "unspoken" rules that insurance adjusters use to evaluate your life.

If you are feeling lost or worried about your current policy, you are not alone. We are going to break down these invisible walls today. You deserve to know exactly what stands between you and your money. Let's look at the things that keep your claim from being a success.

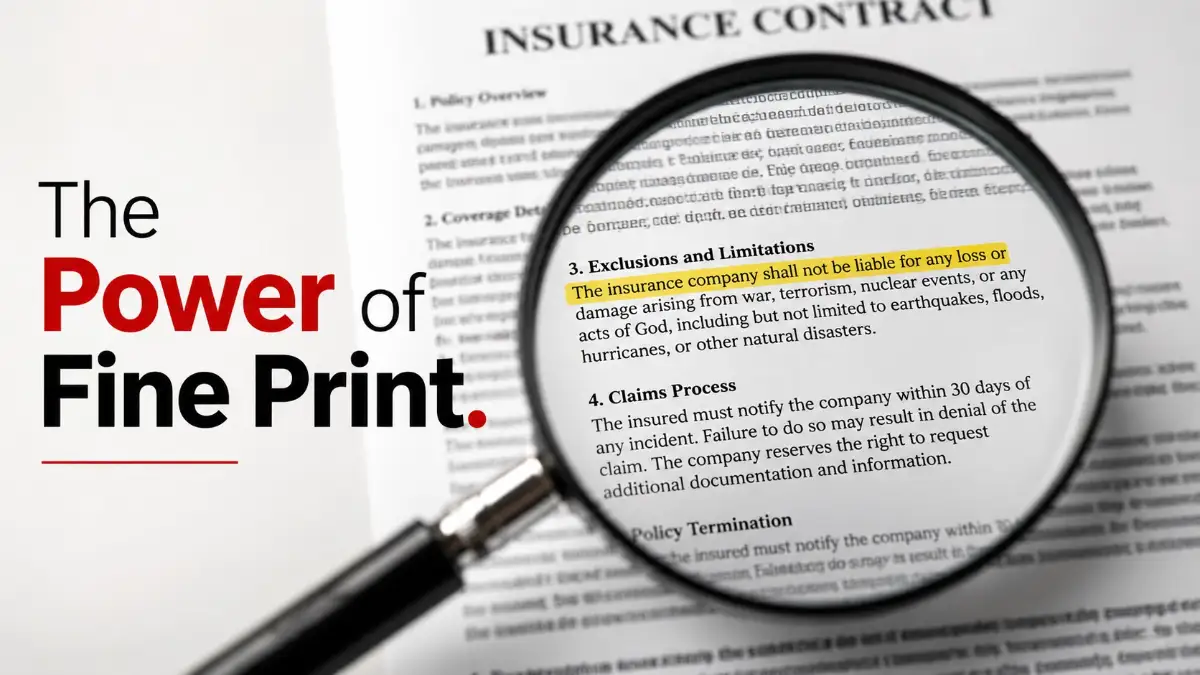

Hidden Traps in the Fine Print You Might Have Missed

Most of us treat insurance policies like "Terms and Conditions" on a website. We just scroll to the bottom and sign. This is the first big mistake. The "Fine Print" is where insurance companies hide the limitations that can ruin your claim.

One major hidden factor is "Gradual Damage vs. Sudden Damage." Most policies cover sudden events, like a pipe bursting. However, if that pipe had a tiny leak for months and you didn't notice, they might call it "maintenance neglect."

If they decide you didn't take care of your property, they will deny the claim. They expect you to be a detective in your own home. It sounds unfair, but it is a standard rule in many contracts.

The Danger of "Non-Disclosure" and Honest Mistakes

When you first signed up for your policy, did you answer every question perfectly? Sometimes, a small mistake during the application stage comes back to haunt you years later. This is known as non-disclosure.

For example, if you forgot to mention a small pre-existing condition on a health policy, or a minor car modification, the company can void your entire claim. Even if that mistake has nothing to do with your current accident!

They look for any reason to show that the "risk" was different than what they agreed to. Honesty is the only policy here. Even a tiny white lie or a simple "I forgot" can lead to a total rejection of your funds.

How Your Home Maintenance Routine Affects Your Check

Did you know that skipping your annual roof inspection could cost you thousands? Insurance is not a replacement for general upkeep. If a storm hits and your shingles were already old and rotting, the company might only pay a fraction of the cost.

They use a concept called "Depreciation." They argue that your roof was already losing value, so they won't pay for a brand-new one. This often catches homeowners by surprise. They expect a full replacement but get a small check instead.

Keep a log of everything you fix. If you hire a plumber, save the receipt. If you trim the trees near your house, take a photo. Documentation is your best friend when you need to prove that you are a responsible owner.

The Secret Impact of "Change in Circumstance"

Life changes fast. You might start a small side business from your garage. Or maybe you decided to rent out a room on a travel website. Most people don't think to call their insurance agent for these things.

However, a change in how you use your property can cancel your coverage. If a fire starts in your garage while you are running a business, your "homeowners" policy might not cover it. They will say you needed a "commercial" policy.

Always update your agent on major life changes. It might increase your premium by a few dollars, but it ensures your claim actually gets paid when you need it.

The Timing Trap: Why Waiting Is a Big Risk

Many people wait a few days or even weeks to file a claim. They want to clean up first or "figure things out." This is a huge error. Most policies have a strict time limit for reporting an incident.

If you wait too long, the insurance company will argue that the damage got worse because of your delay. They might also say it is harder for them to investigate the "true cause" of the loss.

As soon as an event happens, take photos and call your provider immediately. Even if you don't have all the details yet, getting the claim "on the record" is a vital move for your protection.

Understanding the "Excluded Perils" List

Every policy has a list of things it simply will not cover. These are called exclusions. Common ones include earthquakes, floods, or "acts of war." If you live in an area prone to these things, you usually need a separate policy.

A hidden factor here is "Concurrent Causation." This is a fancy way of saying that if two things happen at once—one covered and one not—the company might deny the whole thing.

For example, if a windstorm (covered) and a flood (not covered) hit your house at the same time, you might face a massive legal battle to get a single penny. Review your exclusion list every single year to make sure you don't have a giant hole in your safety net.

The Role of the Independent Adjuster vs. Company Adjuster

When you file a claim, the insurance company sends an "Adjuster" to look at the damage. It is important to remember: that person works for the insurance company. Their job is to save the company money.

They might be very nice and helpful, but their loyalties are clear. Many people don't realize they have the right to hire their own Public Adjuster. This is an independent expert who works only for you.

A public adjuster looks for the hidden damage that the company adjuster might "overlook." They know the language of the policies and can fight for a higher payout. While they take a small percentage of the claim, they often get you much more money in the end.

The Importance of Precise Documentation

If you can't prove it, it didn't happen. That is the motto of the insurance world. If you claim you lost a $2,000 laptop in a fire, but you don't have a receipt or a photo, the company might only give you $500 for a "standard" model.

Digital backups are a lifesaver. Take a video of every room in your house once a year. Open the drawers. Show the brands of your electronics. Store this video in the cloud (like Google Drive or iCloud).

If your house is destroyed, you won't have to rely on your memory. You will have a visual inventory that is very hard for an insurance company to argue with. This simple 10-minute task can save you from a massive headache later.

Why Your Credit Score Might Be Part of the Problem

This is one of the most "hidden" factors of all. In many places, insurance companies use your credit-based insurance score to help decide your claim's "risk level."

While a bad credit score might not get a claim denied directly, it can make the process much harder. It might lead to more "investigation" into your claim because the company sees you as a higher financial risk.

Maintaining a good credit score doesn't just help with loans; it actually smooths the path for your insurance interactions. It builds a profile of "responsibility" that works in your favor during a dispute.

Thoughts for This Part

Insurance is a tool, but you have to know how to use it. You can't just buy a policy and forget about it. You must stay active, stay honest, and stay informed.

We have covered the big hidden traps like maintenance, fine print, and timing. These are the foundations of a successful claim. In the next part, we will look at how to talk to adjusters and the legal steps you can take if things go wrong.

Stay alert and keep your documents ready. Your financial peace of mind depends on the details you handle today. You have the power to ensure your claim is approved, but only if you know the secrets of the game.

Mastering the Art of Claim Negotiation and Documentation

Now that we have covered the basics of what hides in your policy, let’s talk about how to take control of the situation. Getting a claim approved is not just about having insurance. It is about how you present your case to the person holding the checkbook.

Think of an insurance claim like a court case. You are the plaintiff, and the insurance company is the judge. To win, you need more than just a story; you need undeniable evidence. Most people fail because they provide vague information.

One of the best pro-level secrets is keeping a "Claim Diary." From the very minute something goes wrong, start writing. Record the time, the weather, and exactly what you saw. If you talk to anyone from the insurance company, write down their name, the time of the call, and what they told you.

The Secret Power of the "Paper Trail"

Why is this so important? Because insurance adjusters handle hundreds of files. They forget details. If you can say, "On Tuesday at 2 PM, Sarah told me that my water damage was covered," you have the upper hand. It shows you are organized and serious.

I always suggest that you communicate through email as much as possible. If you have a phone call, send a follow-up email right after. Say, "Just to confirm our conversation, we discussed X, Y, and Z." This creates a permanent record that cannot be deleted or "forgotten."

When you are filling out forms, the language you use matters immensely. Sometimes, using the wrong word can change the meaning of your claim. It helps to spend some time deciphering insurance jargon so you don't accidentally say something that limits your payout.

Using Independent Quotes as Leverage

Never assume the insurance company’s repair estimate is the only one. They often use software that picks the lowest possible prices for materials and labor. This might not reflect the actual cost in your local area.

Before you accept their offer, get three independent quotes from local contractors or mechanics. If their prices are higher than the insurance company's offer, send those quotes to your adjuster. Ask them to explain why their estimate is so much lower.

Most of the time, the adjuster will meet you in the middle or match the higher price if the contractor explains the technical reasons. This simple step can add thousands of dollars to your final settlement. It shows the company that you know the market value and won't be pushed around.

The Strategy of "Pre-Damage" Evidence

The biggest struggle people face is proving what they owned before the loss. If your TV is stolen, the company might try to give you the price of a cheap, basic model. But what if you had a high-end OLED screen?

If you have a photo of the serial number and a picture of the TV working in your living room, they have to pay for that specific quality. I recommend doing a "home walkthrough" video every six months. Just walk through your house with your phone camera on.

Open your closets and your kitchen cabinets. Mention the brands of your appliances. This video is your ultimate insurance policy. It proves the condition of your home and the quality of your belongings. If a fire or storm hits, this video is worth its weight in gold.

How Your Financial Health Plays a Role

You might not realize it, but the way you manage your money can affect how insurance companies view you. While it’s not a direct reason for denial, having a solid financial background makes you look more credible. If you've ever wondered why banks say no to loans, some of those same logic points apply to how insurance risks are calculated.

Maintaining a healthy credit utilization ratio shows that you are responsible. Insurance companies often look at "Insurance Scores," which are similar to credit scores. A higher score often leads to smoother claim processing because you are flagged as a "low-risk" client.

Fatal Errors That Shut Down Claims Instantly

Even with the best tips, a single mistake can ruin everything. These are the "pitfalls" that catch people when they are already stressed and tired. I have seen honest people lose their entire claims because of a simple sentence or a quick decision.

The most common mistake is admitting fault too soon. In the heat of the moment, like right after a car accident, many people say, "I'm so sorry, I didn't see you!" While this feels like the polite thing to do, the insurance company will use it as a confession.

They will argue that you admitted liability. This can lead to a denied claim or a massive increase in your future premiums. Even if you think you might be at fault, wait for the official investigation. Stick to the facts and let the professionals decide.

The Danger of "Quick Fixes" Before Inspection

When your roof is leaking, your first instinct is to fix it. You want to protect your home. However, if you throw away the damaged materials before the insurance adjuster sees them, they might deny the claim.

They need to see the "cause of loss." If you replace the broken pipe and throw the old one in the trash, you have destroyed the evidence. Always keep the damaged parts until the adjuster gives you the green light to toss them.

If you must make emergency repairs to prevent more damage, take 50 photos first. Take photos of the hole, the water, the broken piece, and the surrounding area. Keep the receipts for any materials you bought for the temporary fix. This proves you were trying to mitigate the loss, which is actually a requirement in most policies.

Recorded Statements: The Silent Claim Killer

Shortly after you file a claim, an adjuster will call and ask to record your statement. They might sound very friendly, like they are just trying to help you faster. Be very careful.

These recorded statements are often used to find inconsistencies in your story. If you say one thing on day one and a slightly different thing on day five, they might flag your claim for fraud. You are not legally required to give a recorded statement immediately.

You have the right to say, "I am not ready to give a recorded statement yet. I want to review my notes first to make sure I am accurate." This gives you time to calm down and ensure your story is clear and consistent. You can even check with organizations like the National Association of Insurance Commissioners to see what your rights are in your specific area.

Taking the First Offer Without Questioning

The insurance company wants to close your file as quickly and cheaply as possible. Often, the first check they offer is a "low-ball" amount. They hope you are desperate for the money and will sign the "Release of Liability" form.

Once you sign that form and cash the check, the claim is over. If you find more damage a week later, you cannot go back for more money. Never rush to sign the final release.

Wait until you are 100% sure that all the damage has been found and repaired. If the contractor finds more issues during the repair process, you can ask for a "supplemental" payment. But this is only possible if you haven't signed your rights away yet.

Ignoring the "Proof of Loss" Deadline

Every insurance policy has a clock ticking. There is a specific document called a "Proof of Loss" form that must be submitted within a certain number of days. If you miss this deadline, the company can legally walk away from the claim.

Many people get caught up in the repairs and forget the paperwork. Don't let this happen to you. Mark the deadline on your calendar in bright red. If you think you might miss it, ask for a written extension from your adjuster. According to the Consumer Financial Protection Bureau, staying on top of your deadlines is one of the most important parts of managing any financial contract.

Your Future-Proof Action Plan for Financial Safety

You have the power to turn a stressful situation into a manageable one. Dealing with insurance is about being proactive instead of reactive. It’s about knowing that the "hidden factors" are only hidden if you don't look for them.

Starting today, take a few small steps. Locate your policy and read the "Exclusions" section. Take a quick video of your home. Save your insurance agent's number in your phone. These small actions create a shield around your finances.

If you ever find yourself facing a denied claim, don't give up. You have the right to appeal. You have the right to ask for a supervisor. You have the right to fight for what you have paid for. You are a paying customer, and you deserve the protection you were promised.

Believe in your ability to handle this. You are now armed with the knowledge that most people lack. Use it to protect your family, your home, and your future. You've worked hard for what you have—make sure your insurance works just as hard for you.

Disclaimer: This article is for informational purposes only and does not constitute legal or professional financial advice. Insurance laws and policy terms vary by region and provider. Always consult with a licensed insurance professional or a legal expert regarding your specific situation and policy details.